Receiving business payments, particularly from overseas partners, often involves challenges such as currency exchange issues, processing delays, and limited payment visibility. As global operations become the norm, companies are seeking more efficient, secure, and transparent ways to manage incoming funds.

Outdated systems frequently fail to meet these modern demands, creating unnecessary complications. A trusted solution is the use of IBANs (International Bank Account Numbers), which offer a streamlined and consistent method to receive business payments across borders, enabling quicker transactions and greater financial oversight for businesses worldwide.

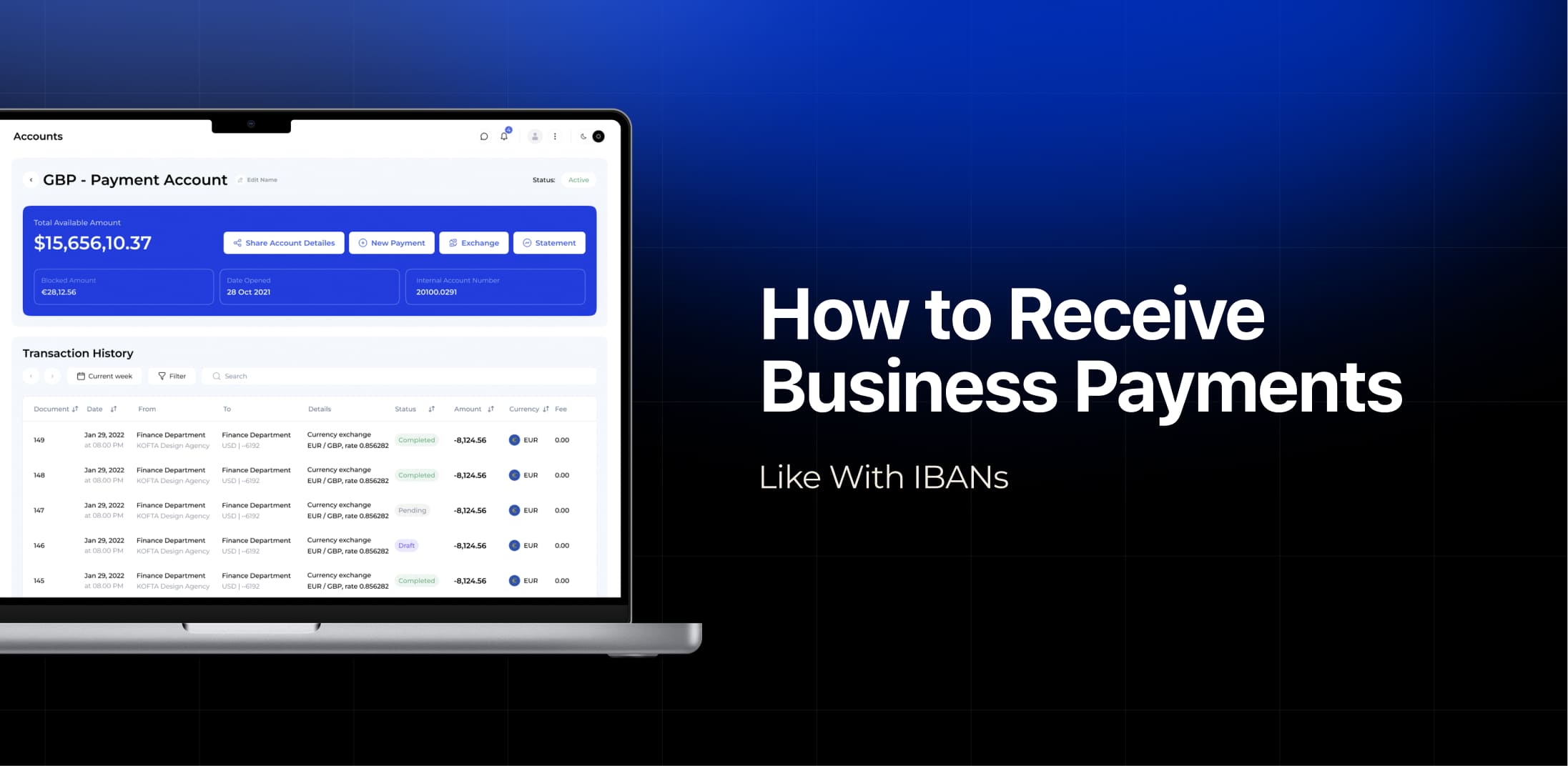

What Is an IBAN and Why It Matters for Business

An IBAN (International Bank Account Number) is an internationally recognized format designed to uniquely identify bank accounts across national borders. It typically consists of a country code, two check digits, and a sequence of alphanumeric characters that represent the specific bank and account. Commonly used throughout Europe, the Middle East, and other regions, IBANs simplify and secure cross-border payment processes.

By providing a consistent structure, they minimize input errors, accelerate transaction times, and ease account reconciliation. For companies, having access to a multi currency IBAN offers a reliable way to receive global payments swiftly and accurately. This not only helps reduce failed transactions but also projects a more professional image to international partners, strengthening business relationships and supporting global financial integration.

Benefits of Receiving Payments via IBANs

Receiving business payments through an IBAN delivers a range of benefits that strengthen both financial operations and security. First and foremost, the standardized structure of an IBAN enhances security by minimizing the chances of misdirected payments and fraudulent activity. When it comes to speed, IBANs facilitate quicker processing, especially in the SEPA (Single Euro Payments Area) zone, where transactions are typically settled within one working day.

The traceability of IBAN transactions also streamlines reconciliation, making it easier for businesses to manage incoming funds and maintain clear financial records. Moreover, IBANs help businesses stay compliant with global regulations, supporting Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols.

From a cost-efficiency perspective, using IBANs, particularly within supported networks like SEPA, can significantly reduce international transfer fees. In short, IBANs offer a secure, fast, and cost-effective solution for businesses handling cross-border payments.

Setting Up an IBAN to Receive Payments

To receive payments through an IBAN, businesses can obtain one via traditional banks, modern fintech platforms, or regulated payment service providers. Each channel offers distinct advantages – fintech companies, for example, often deliver quicker onboarding and greater flexibility. Setting up an IBAN typically requires company registration documents, KYC verification, and in some jurisdictions, proof of a local business presence.

When evaluating providers, it’s important to consider factors like multi-currency capabilities to support international clients, an intuitive online platform for seamless account control, and API integration to streamline operations. Selecting the right IBAN solution not only simplifies payment workflows but also enhances financial clarity and supports international growth with minimal friction.

Multi-Currency IBAN Account: A Smarter Way to Get Paid Globally

Multi-currency IBANs offer businesses a flexible way to receive payments in multiple currencies, like USD, EUR, and GBP, using just one account. Unlike traditional IBANs, which are usually limited to a single currency, multi-currency IBANs simplify global payment collection by consolidating different currency transactions into a unified system.

This is particularly advantageous for e-commerce businesses, SaaS companies, and remote-first organizations operating across international markets. Accepting funds in the sender’s original currency helps avoid automatic conversions and related fees. As a result, companies benefit from greater cost control, clearer financial reporting, and smoother cash flow management across different regions.

Alternatives to IBANs for Receiving Business Payments

Although IBANs are a popular choice for international payments, businesses may also encounter other formats, such as using a Bank Identifier Code (BIC) alongside a traditional account number. This method remains common, especially in countries outside the SEPA zone. However, such transfers may involve longer processing times or higher fees, depending on the banks involved and the destination country.

Virtual accounts, provided by neobanks or payment service providers (PSPs), offer a modern, digital solution that streamlines payment handling and simplifies reconciliation. Cryptocurrency wallets allow fast, decentralized transactions with minimal fees, though their price fluctuations can introduce financial risks.

Additionally, fintech-enabled local bank accounts in foreign markets let companies receive payments like a local entity, cutting expenses and enhancing convenience. Each option presents unique benefits, making it important for businesses to choose based on their specific operational needs and target markets.

Conclusion

IBANs serve as an effective and secure method for managing international business payments. Businesses should consider providers such as PaySaxas, which deliver both direct and multi-currency IBAN options to streamline global transactions. Establishing a robust payment infrastructure with PaySaxas supports smooth scalability and long-term international expansion.